The History of ProAssurance Is a History of Mergers and Acquisitions

Birthdays are straightforward for individuals, but settling on one for an organization, as we recently did to celebrate ProAssurance’s 50th, can be complicated.

Is a company “born” when the entrepreneur has the Eureka! spark of inspiration, or does it at least have to be sketched out on the proverbial bar napkin? If the date is “official,” does it need to tie back to a government body affirmation of your existence, like the date of your business license or a certificate of authority? What if the state approves you Monday but the city or county takes longer? Maybe it’s the date of the first board meeting or some official act after all the red tape is sorted?

If the business is open to the general public, like a retail store or a restaurant, maybe it’s the day the doors were first open for business (never mind last week’s “soft launch” to test the point-of-sale system or the fact that the mayor couldn’t schedule the ribbon cutting photo op until the next week). For professional services, maybe it’s your first sale. Does an insurance company that hasn’t yet sold a single policy really exist?

And those are the easy questions! It gets a lot more complicated once your company starts engaging in mergers and acquisitions. If a firm you acquire was “born” before you, do you get older or do they get younger?

What’s clear for us at ProAssurance is that at some point, indeed at several points over the next 18 months, we will have cause to celebrate our 50th birthday. Therefore, we are declaring 2026 as “Our 50th Year!”

Officially our “birthday” is October 1, 1976, which is the date of incorporation for the Mutual Assurance Society of Alabama, now known as ProAssurance Indemnity Company, Inc. The many competing dates that also would have been great choices include February 14, 1977, the date we were licensed by the state of Alabama, and April 15, 1977, the date our first policy became effective.

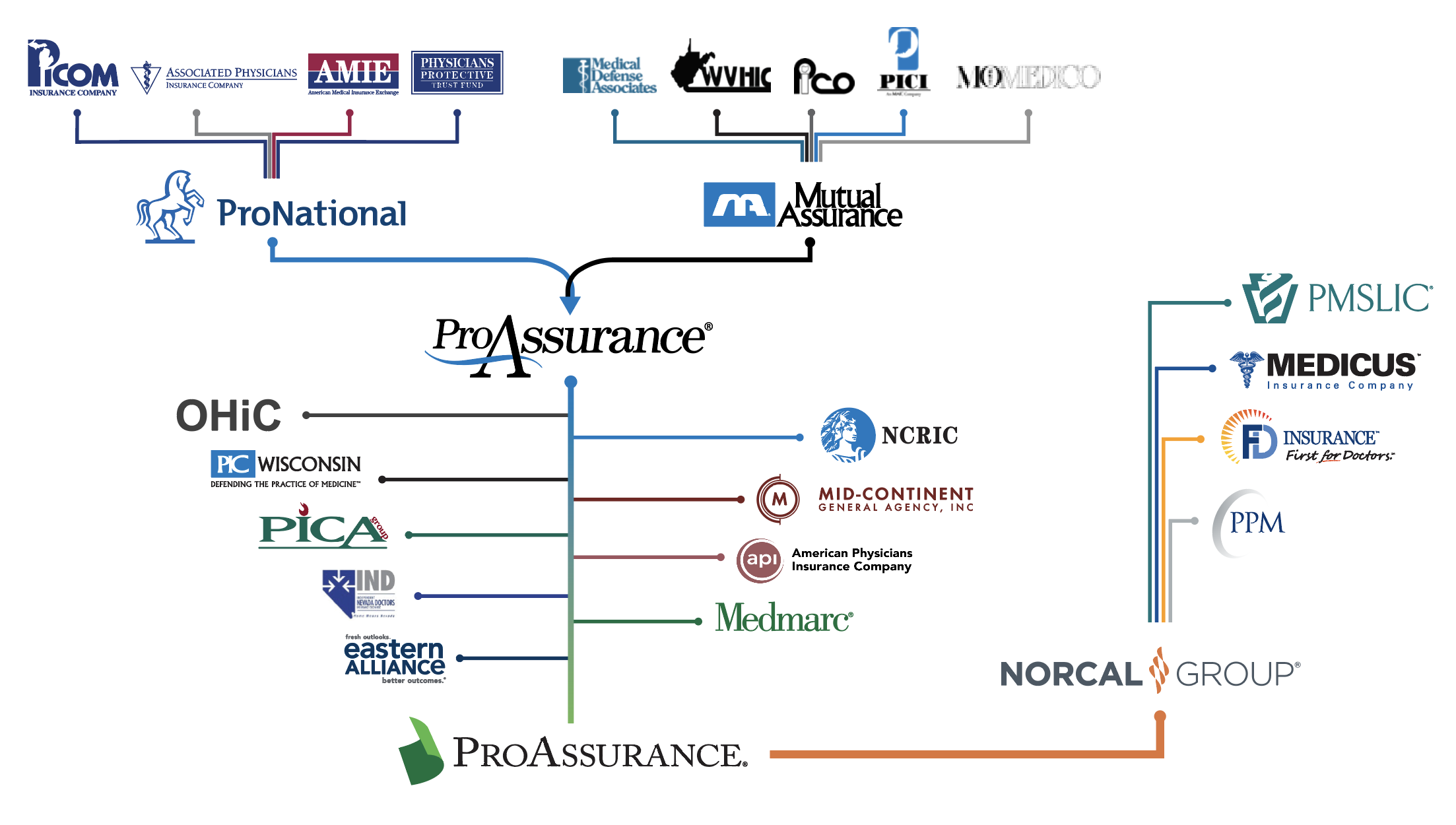

Once you start contemplating birthday time travel via mergers and acquisitions, ProAssurance may already be 51, or even 76! The ultimate predecessor company to ProNational (part of the merger that formed modern-day ProAssurance) was PICOM, which privatized Michigan’s state fund, the Brown-McNeely Insurance Fund. The act that created Brown McNeely was passed in the 1975 legislative session, and the fund began issuing coverage on January 1, 1976. But in the 1990s, PICOM bought MEEMIC, an auto insurer, that was incorporated August 10, 1949. That company was sold in 2009, arguably de-aging us by 26 or 27 years. Yes, it can get complicated.

One thing that’s simple for us at ProAssurance is the mission and focus of our last 50 years—and the next 50. Our company, and numerous other medical malpractice insurance companies also celebrating their 50ths, were formed from an insurance crisis in the 1970s. Claims frequency and severity against physicians were rapidly escalating, making commercial insurance either unavailable or unaffordable. In Alabama, a group of visionary physicians partnered with the state medical association to address the crisis by forming a mutual insurance society. This same pattern of mutual formation in partnership with organized medicine was happening in numerous other states in those years.

For the next 50 years, defending the practice of good medicine remained our mission. While the company structure, practices, names, and product offerings adjusted over the years to adapt to market demands, protecting the interests of our insured physicians remained our focus, and we’re proud of our accomplishments today.

To all our customers, agency partners, defense attorneys, employees, medical association partners, and other stakeholders past and present, thank you for a terrific half-century.

The 50th anniversary logo and this announcement launch our 50th anniversary campaign, and throughout this year we’ll be celebrating key moments from the past and those who made them happen. We look forward to sharing those moments here online as we venture into our next 50.

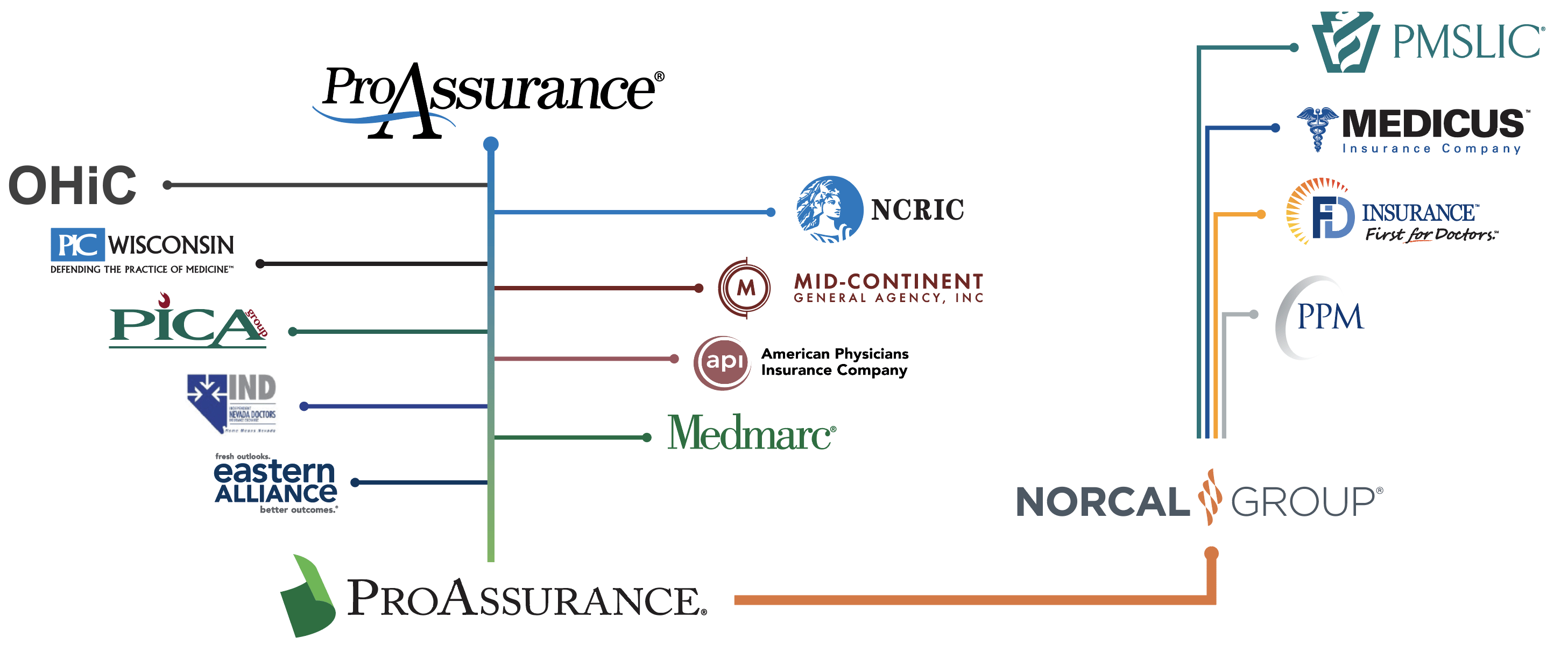

ProAssurance’s Journey of Growth Through Strategic Mergers

The third, and penultimate, chapter in ProAssurance’s remarkable story begins with the successful conclusion of the 2001 merger between Medical Assurance and Professionals Group, the parent of ProNational Insurance Company.

The third, and penultimate, chapter in ProAssurance’s remarkable story begins with the successful conclusion of the 2001 merger between Medical Assurance and Professionals Group, the parent of ProNational Insurance Company.

Bringing together the footprints of both companies resulted in a super-regional organization with the financial strength, geographic reach, and sophisticated expertise to meet the liability needs of a rapidly changing healthcare delivery system.

Derrill Crowe, M.D., who was Chairman and Chief Executive Officer of the new company, says, “There was a strong commitment among senior management to ensure that ProAssurance maximized the potential advantages gained through the merger. I’d like to think much of that came from the spirit of cooperation that Vic and I demonstrated. There was some of the usual friction that comes from merging two companies and their cultures, but we all wanted it to work. And remember, both companies, each with different strengths, shared a common commitment to serving our policyholders and our distribution partners.”

“I think the merger went very well; we did everything basically right, and over the course of the next ten years, the transaction certainly proved itself financially,” said Vic Adamo, the former President and Chief Executive Officer of Professionals Group, who became President and Chief Operating Officer of ProAssurance. He added, “While there was some attrition as a result of the integration of the two companies, an important measure of the success of the merger was that almost all of the C-suite officers from both Medical Assurance and Professionals Group spent the remainder of their careers with the combined company.”

Having demonstrated its successful integration, the new company moved to take advantage of its standing in the market through a succession of capital-raising activities.

In late 2002, ProAssurance sold just over three million shares of common stock, raising approximately $6.5 million to support continued business expansion and to ensure the company maintained the financial strength required to retain its ratings as it pursued new opportunities to insure large, complex risks.

That stock sale was followed in mid-2003 by the issuance of $105 million in convertible debentures. The proceeds helped the company eliminate debt, strengthen the finances of its subsidiary insurers, and expand its insurance operations.

In 2004, ProAssurance issued $46 million of trust-preferred securities. The funds ensured that the company would remain on a strong financial footing and be able to sustain its growth trajectory.

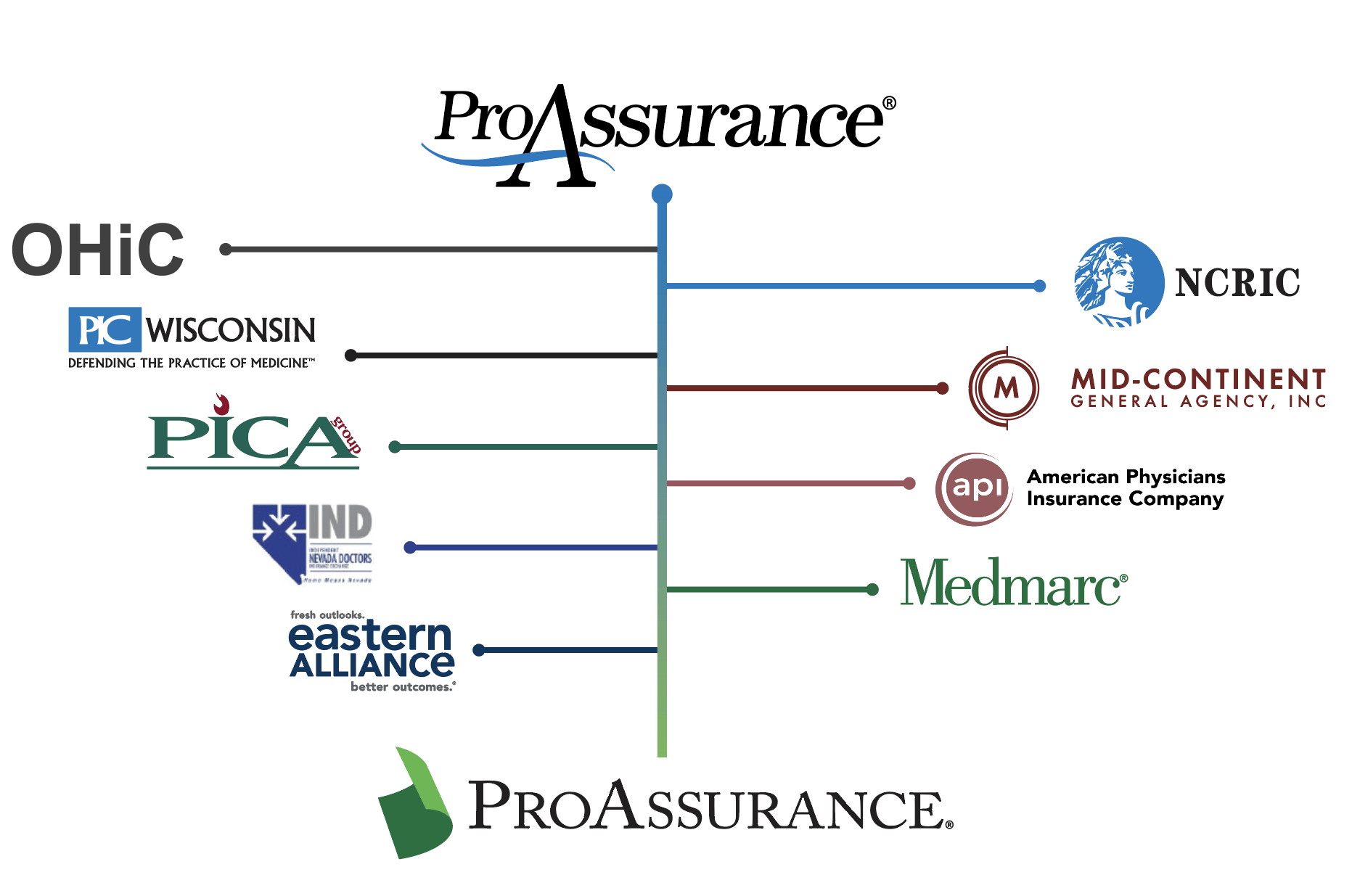

Both Medical Assurance and ProNational had grown prior to the merger through de novo expansion and a number of strategic acquisitions. That trend continued following the merger.

Already a leader in the Midwest, ProAssurance in 2004 purchased the renewal rights to Ohio Hospital Insurance Company’s physician, hospital, and healthcare facility business in Indiana, Illinois, Kansas, Kentucky, and Wisconsin.

ProAssurance remained active and in 2005 acquired the NCRIC Group, a policyholder-founded company that had converted to a mutual-holding company with publicly traded stock. The NCRIC transaction strengthened ProAssurance’s footprint in Washington, D.C., and surrounding states.

In 2006, ProAssurance acquired Physicians Insurance Company of Wisconsin (PICWIS), which primarily served its home state but also had business in surrounding states and in Nevada through a prior transaction. With the acquisition of PICWIS, all the Midwestern companies that shared a founding legacy through Physicians Insurance Company of Ohio were now part of ProAssurance.

The market was not standing still, and other companies were expanding with the same rationale and imperative that drove ProAssurance. One of the leaders was California-based NORCAL Mutual Insurance Company, which would become part of ProAssurance much later in the story.

NORCAL, as the acronym implies, served primarily physicians in Northern California. The company emerged from the malpractice availability crisis that prompted the creation of other policyholder-founded companies across the country. In NORCAL’s case, eight county medical societies were the sponsoring organizations, and it insured just over 3,000 physicians at the outset.

Given the size of the California market, NORCAL largely operated within the state, where it competed with similar companies based in Southern California. Over time, however, the need to grow and diversify its insurance base drove NORCAL to expand into surrounding states, eventually reaching as far afield as Alaska and Hawaii.

NORCAL’s first significant acquisition came in 2002, when it acquired the Pennsylvania Medical Society Liability Insurance Company (PMSLIC), which had been created during the medical liability crisis of the late 1970s.

Veteran medical liability insurance executive Scott Diener was named by NORCAL to assume the leadership role at PMSLIC. Diener, who would later become President and Chief Executive Officer of NORCAL, says, “Like many of the professional liability companies at the time, we felt that we needed scale to be successful long term and to be able to cover the spectrum of healthcare delivery, from individuals and small groups to larger organizations.”

The changing medical-legal landscape and changes in healthcare prompted a move that surprised nearly everyone. In early 2007, Dr. Crowe, who had guided Mutual Assurance at its creation and through its ascension to the top ranks of the medical liability industry, announced that he was stepping away from his role as Chief Executive Officer.

Dr. Crowe recalls the thought process this way: “Healthcare was changing rapidly, and the legal system was undergoing another detrimental shift in the thinking of juries and the way state laws were structured, particularly in Florida. I wanted someone who understood the law and the ethos of the company, but who could make the changes that I felt might be needed.”

Dr. Crowe’s handpicked successor was Stan Starnes, ProAssurance’s lead defense attorney who knew ProAssurance because of his long association with the Company. Starnes, and the network of skilled defense attorneys he helped the company recruit, had vindicated Crowe’s innovative approach to handling claims and earned the company a remarkably loyal following among its insureds.

Starnes recalls the conversation clearly: “He said, ‘Stan, we’ve built an enormously successful company, but I’m almost 70. I’m tired. I’m ready to quit. I’m either going to name you the new CEO or I’m going to have to think about selling the company.’ I told him I had to think about it, and we reconvened a week or so later. After a long, frank conversation, I decided to take it.”

“I didn’t want to see him sell the company. I believed the company was playing a very important role in making the world safe for physicians and others in healthcare to practice medicine without the threat of a devastating lawsuit. And I knew that if we sold the company, whoever bought it would run it like a regular insurance company, not like the organization it had become. It was the right decision for me. It was the right decision for him, and it was the right decision for the organization.”

Crowe would remain as Chairman until 2008, but the DNA he injected into the company is woven into the fabric of ProAssurance to this day.

Acquisitions continued under Starnes’s leadership, bolstering not only the traditional medical liability business but also expanding ProAssurance’s vision of the company as it prepared to address the tangential risks increasingly intertwined with modern medicine.

The first acquisition under Starnes’s leadership came in January 2009, when ProAssurance acquired Mid-Continent General Underwriters, which brought expertise in insuring allied health providers and added hundreds of policyholders.

In 2009, ProAssurance acquired the Podiatry Insurance Company of America (PICA) in a sponsored demutualization that brought the largest insurer of podiatrists in the country into ProAssurance and expanded its umbrella to chiropractors and acupuncturists. PICA itself had grown through acquisitions, having acquired PACO Assurance Company, Inc., in late 1998, Dependable Protective Mutual in 2000, and OUM in 2001.

ProAssurance entered the dynamic Texas market in 2010 with the acquisition of publicly traded American Physicians Service Group, based in Austin, Texas. That transaction also expanded the company’s business in Arkansas and Oklahoma.

Austin became something of a medical liability insurance hub. In 2011, NORCAL acquired Medicus Insurance Company, an MPL start-up also based there. The transaction dramatically enlarged NORCAL’s footprint, as Medicus operated in 34 states and had built a strong agent network.

In 2013, ProAssurance acquired Independent Nevada Doctors Insurance Exchange (IND), which, combined with business gained through the PICWIS transaction, made ProAssurance the largest medical liability insurer in that state.

Looking further afield within the healthcare-related space, ProAssurance in 2013 acquired Medmarc Insurance Group, one of the nation’s leading providers of liability insurance for medical products and life sciences. The scope of insurance products available to the company’s distribution partners continued to expand.

Another leap forward came the following year, when ProAssurance acquired Eastern Insurance Holdings, a significant provider of healthcare-centric workers’ compensation insurance that also demonstrated expertise in alternative risk transfer through self-insurance and captive programs.

While not initially expected by the market, the benefits of the transaction soon became clear: coverage for two of the most difficult lines of insurance was now available through a single company with a depth of expertise unavailable in the broader commercial market.

2014 was also the year ProAssurance became multinational as the majority capital provider for Syndicate 1729 at Lloyd’s of London. This provided access to an innovative avenue for insuring one-off risks and allowed ProAssurance to participate in select opportunities outside the United States. While the venture ultimately did not achieve the level of success envisioned, it further demonstrated the company’s forward-thinking approach to professional liability.

The next major transaction belonged to NORCAL, which purchased FD Insurance, then the largest insurer in Florida. The all-cash transaction added approximately 2,200 healthcare providers in Florida and Georgia and strengthened NORCAL’s assets by more than $80 million.

NORCAL followed that acquisition with the purchase of Preferred Physicians Medical Risk Retention Group (PPM), an anesthesiologist-founded, specialty-specific insurer.

Consolidation in the medical professional liability space continued, but Scott Diener, by then President and Chief Executive Officer of NORCAL, notes that willing sellers were becoming increasingly scarce: “Continuing to acquire or combine with smaller or similarly sized companies was very definitely a strategy—and arguably the preferred strategy—for us. But at some point, every company that wanted an exit or needed to leave the business had already done so.”

Further, Diener explains that changes in physician practice ownership began to erode the claims philosophy of traditional MPL insurers: “As practices consolidated and hospitals took over, the importance that physician-owned companies attached to provisions like the consent to settle clause began to diminish. Administrators holding the purse strings were less concerned and sometimes even found it objectionable to pay for policies built around values that mattered to physicians, but not necessarily to an administrator’s vision of the bottom line.”

Everything appeared to be pointing toward the combination that would bring NORCAL into ProAssurance. Initial conversations had begun, but first there was another change at the top.

In 2019, Stan Starnes decided it was his time to relinquish his role as CEO. He says, “I was weeks away from my 71st birthday and completing my 12th year as the CEO of a public company. There is a reason the average tenure of a public company CEO is about half of that.”

During each year of Starnes’s tenure, ProAssurance was named one of the top 50 casualty insurance carriers in the United States out of a universe of more than 3,500 carriers—a testament, he says, to the people of ProAssurance. “Thanks to the hard work of our executive team and employees across the country, I felt that we had accomplished what we set out to do 12 years earlier. The timing was right.”

Longtime ProAssurance executive Ned Rand was named to succeed Starnes, who remained Executive Chairman of the Board until 2022, long enough to lead the Board through completion of the NORCAL transaction and the challenges of the COVID-19 pandemic.

Rand joined ProAssurance in 2004 after stints in public accounting and financial leadership roles within the insurance industry. Having risen through the executive ranks—as Senior Vice President of Finance, Chief Financial Officer, Chief Operating Officer, Executive Vice President, and now President and Chief Executive Officer—he recalls the excitement he felt with the transition.

“I had a real sense of excitement because of the people we had in leadership, the team of employees we had assembled, and the opportunity ahead of us. With that excitement came a sense of optimism.”

By the time Rand assumed his leadership role, discussions with NORCAL were already progressing. “We were still a long way from getting the transaction done when I moved into the president’s role. But I remember a pivotal meeting where we ultimately solidified things with the NORCAL board.”

Diener says ProAssurance offered everything the NORCAL Board had identified as essential to a transaction. From his perspective, the combination honored NORCAL’s commitment to policyholders and ensured their protection going forward. “The Board was very pleased with the company. We believed we were top tier, but we asked ourselves, ‘Are we able to serve our changing, large healthcare-system policyholders effectively? And are we using our policyholders’ capital effectively?’ The answer to both questions was no. That’s what led us to combine with ProAssurance.”

He continued. “We were using capital contributed by our original and early customers to serve newer, larger customers. When we weighed the alternatives and considered the opportunity both to honor policyholders and to meet the needs of future customers, consolidation with ProAssurance was the clear answer.”

The acquisition was completed in May 2021. The two policyholder-founded companies that were started to serve a few thousand physicians in Alabama and California have united through dozens of transactions to become a leading national force in the medical liability industry.

The numbers tell a quantitative story: tens of thousands of policies in force and a strong network of hundreds of distribution partners. But there is a qualitative story that’s told in the legacy of service to policyholders, agents, and brokers. It is, according to Ned Rand, the story of an enduring corporate culture, “I'm probably most proud of the culture of the organization. It is about everybody working together while, at the same time, respecting and valuing the uniqueness of each individual within the organization. That’s what has allowed us to perpetuate the values that were present in our company at our founding five decades ago.”

Now a new chapter is ready to be written with the agreed-to acquisition of ProAssurance by The Doctors Company (TDC). ProAssurance shareholders have approved the transaction, and regulatory approval is expected in the first half of 2026. The legacy will endure, given TDC’s policyholder focus and broad insurance capabilities.

.png?width=300&name=MicrosoftTeams-image%20(28).png)

You Can’t Change History … But You Can Try to Change Perspective

History is fascinating, and sometimes worth celebrating—like ProAssurance turning 50 and reflecting on its impact in the industry.

And then there’s the history you wish people would forget. I’m talking about prospects and clients who blame you for someone else’s past mistakes. Sometimes you can fix it, and sometimes you can’t.

The Doctor Who Hated Me (Without Knowing Me)

Throughout my sales career, I’ve always been persistent. I’d show up with purpose, a smile, and keep coming back. Most surgeons, even if they were busy, would at least acknowledge me.

Except for one. Dr. Bernard. After a year in my new territory, he was the only surgeon I hadn’t met. I’d stop by his office, leave a card, drop off literature, repeat. Crickets.

Then one day, as I headed into his office, he was walking out. I stopped, smiled, extended my hand, and said, “Dr. Bernard! I’m Mace with XYZ Orthopedics. Great to finally meet you.” He didn’t stop. Didn’t slow down. Didn’t even pretend he might shake my hand. He just glanced back and said flatly in his South African accent: “I have absolutely no interest in meeting you.” Then he turned fully around and delivered the knockout blow:

“I trained on your company’s products as a resident. When I opened my practice, I never saw a sales rep. To me, your company doesn’t exist. Don’t come back.”

And off he went.

I Tried Everything

I ignored the doctor’s order not to return and kept trying. I’d leave product literature, scientific papers, and even donuts. I even had my manager send the doctor a formal letter of apology for the company’s past failure to acknowledge him.

Nothing changed.

One morning, I noticed Dr. Bernard in the OR locker room and, figuring I had nothing to lose, confronted him. “Dr. Bernard, forgive me, but you’ve been blaming me for something that happened long before I was here. I’m trying to make it right. Can we at least talk?”

His response was short and final. “I hate your company. I’ll never use your products. Stop wasting your time.”

So … I did.

The Lesson

You can’t rewrite history for someone who refuses to open the book. No level of sincerity, logic, or even donuts will change them (although his staff appreciated the goodies). But before you give up, here are things worth trying (that work with most reasonable people):

1. Acknowledge the past—even if it wasn’t your fault.

2. Apologize sincerely and personally—not corporately.

3. Explain what’s changed—people, processes, results.

4. Be consistent—it wins most people over in time.

5. Ask for a clean slate—many will give it.

6. Know when to move on—there are some battles you won’t win.

Keep Looking Forward

You can’t change the past—whether it’s industry history, corporate history, or circumstances that existed before you arrived. But you can choose how that history informs what comes next.

As ProAssurance marks 50 years, its history becomes a foundation of trust. Carry it with you into the new year, focusing on clients who are ready to adapt to the changing demands of healthcare and liability, while providing patient care with confidence.

As for any Dr. Bernards along the way, wish them well and move on. The future is built with those willing to move forward together.

|

Written by Mace Horoff of Medical Sales Performance. Mace Horoff is a representative of Sales Pilot. He helps sales teams and individual representatives who sell medical devices, pharmaceuticals, biotechnology, healthcare services, and other healthcare-related products to sell more and earn more by employing a specialized healthcare system. Have a topic you’d like to see covered? Email your suggestions to AskMarketing@ProAssurance.com. |

Risk Management Updates

NEW RISK OFFERING:

Resident Rundown Podcast

This podcast series, hosted by Barbara Hunyady, JD, CPHRM, covers the medical malpractice insurance concerns on the minds of residents, fellows, and other early-in-career doctors. These six episodes cover topics such as when and how to get malpractice insurance, how premiums are calculated, what happens when you’re in a lawsuit, how to protect your personal assets, and how to avoid getting sued in the first place.

- When and how to get malpractice insurance

- How premiums are determined

- What happens when you’re in a lawsuit

- How to limit personal asset exposure

- How to avoid lawsuits

Episodes are available on Spotify, Apple Podcasts, and iHeartRadio. You can also browse all of the episodes on the Risk Management website.

The estate of an 80 YOF alleged that the rehabilitation facility failed to assess, monitor, and document skin integrity, nutritional intake, and repositioning practices, resulting in the development and progression of pressure ulcers, infection, and subsequent death.

Read the issue

In this episode, host Lesley Lopez-Viner discusses medical malpractice lawsuit defense with attorney Bill Chamblee. They explore the evolution of courtroom dynamics, the strategies plaintiff attorneys employ, and the trust jurors place in healthcare providers. Bill shares insights on the rise of nuclear verdicts, the impact of life care plans, and offers risk management advice for healthcare professionals.

Read the issue

Medical assistants can enhance patient care but also pose liability risks if tasks exceed their scope. Proper delegation, supervision, and ongoing competency assessments are essential for patient safety and reducing malpractice exposure.

Read the issue- Communications

- Design

- Digital Marketing