Market Dynamics Presentation

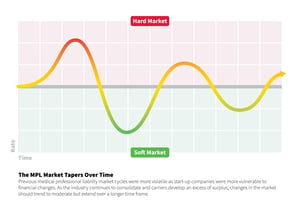

Medical professional liability (MPL) insurance has been in a soft market cycle since 2005. Soft markets are generally characterized by coverage that is widely available, policy terms have been "loose," and price-based competition is common.

However, in a hard market cycle, insurance becomes less available, policy conditions tighten, and premiums increase to stabilize reserves.

Due to the long-tail nature of medical malpractice claims that may take years to resolve, an insurer's long-term financial health is of utmost importance to insureds. ProAssurance was founded in response to the first hard market after it began in 1975, providing stability for our insureds during the next three hard market cycles in the 1980s, 1990s, and early 2000s.

We have created a report that outlines key drivers of the MPL market for use in your sales conversations around hard and soft market cycles and nationwide trends. Download a copy of the presentation at ProAssurance.com/MPLMarketDynamics.

Contact ProAssurance’s Marketing department or your Business Development representative if you have questions about using the presentation.

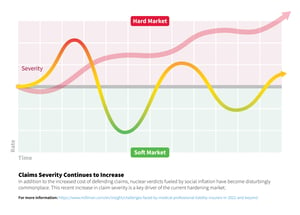

You must educate your insured on the trends going on in the market that are driving the need for higher rates. These involve two inflationary trends, and the first is general economic inflation. Everything costs more for the insurance company, as it does for all of us. One of the largest of those costs is the defending of a claim. Experts charge more, and attorneys charge more as their costs increase. However, the biggest inflationary driver is the loss cost of claims. These have been rising for years, and the increase has accelerated over the past few years, driven by what has been termed social inflation. This describes increases in jury verdicts and plaintiff demands for payment outside of normal inflationary trends. We have higher jury verdicts than ever and more of them across every jurisdiction. Verdicts of $100 million or more are becoming commonplace, driving up settlement costs as plaintiff attorneys become more and more emboldened.

Hard markets do not last near as long as soft markets. A return to price stability will come once premiums adjust to the current claim severity trends and the unpredictability of claims volatility is lowered.

Wise agents should place their clients with a carrier who has a strong balance sheet and a consistent track record for successful claims resolution. They will have prudently navigated the insurance cycles of previous decades.

The MPL market is cyclical. All carriers are going through this, not just us. There are pressures to price accounts responsibly in order to obtain profitability and pay future claims. Agents should review their loss runs and coverage closely to better understand why premiums are where they are.

A hard market is a seller's market. Although we may have leverage to raise rates due to tightening on the availability of insurance, we cannot forget the importance of using this time to build trust and relationships. Our insureds may have limited choices in a hard market, but that will change when the market softens. The relationships, trust, and value we add to their practice can and will help carry us forward and affect retention through the next softening of the market. In addition, we have an impact on claim severity. All of these advantages directly impact the insured's ability to maintain quality insurance during a hard market. The least expensive insurance is not always the best choice.

Increasing premiums are a sign that the MPL industry is responsibly addressing trends related to claim severity. Carriers are expected to apply rate discipline in order to weather the unpredictable cycles of claim volatility. Healthcare providers should look for clear messaging from their carriers on the subject of increasing premiums, and pay attention to the drivers responsible for them. Things that will help restore stability to premiums include preserving effective and proven tort reform measures, obtaining guidance from seasoned agents, and partnering with a financially strong and dependable carrier that takes the long view to insurance cycles.

Are we there yet?! Depends...

Over the years, hard markets challenging affordability and/or availability for medical professional liability coverage have occurred due to various reasons. Factors impacting the current journey toward a hard market in some areas of the country include increased claim severity due to social inflation, eroding tort reform, and the continuing progression in the way healthcare is delivered. Agents can proactively help their clients through a hard market by preparing them for coming changes in premium and policy terms and conditions.

There is a correlation between those states identified with double-digit increases in rates over the past few years and those with tort reform. States with no caps on pain and suffering tend to see higher premiums than those states with caps. Tort reform is constantly challenged each year so it will be interesting to see if more states experience double-digit rate increases in the future.

.png?width=300&name=MicrosoftTeams-image%20(28).png)

No Pressure

Everyone hates pushy salespeople; no agent wants to be perceived as such. It’s time to push your pushy salesperson fears aside! When it comes to healthcare selling, there's no need to apply pressure with prospects and clients because there is something inherent in healthcare that's far more powerful—urgency! I'm not talking about manufactured FOMO-based urgencies like product scarcity or short-term price reductions; I'm talking about fix-it-before-it-becomes-a-problem urgency.

I learned this during my first year in medical sales. My company released a new hospital product—a pressure infuser to increase the delivery speed of intravenous fluids. The infusers available at this time were flexible plastic sleeves that inflated to compress the IV solution, increasing the flow rate.

The infuser I sold was a rigid stainless steel box clamped to an IV pole. Instead of struggling to slide an IV bag into a sleeve, you just opened the door, hung the bag on a hook, and closed the door. Rather than squeezing a hand bulb 10 or 20 times to pressurize the flexible infuser, two to four stomps on a pneumatic foot pump had the fluids flowing. It was superior in every way but presented one obstacle—the price. Whereas the soft infusers sold for about $35, my new device was priced at $595.

I brought the product to an orthopedic surgery I was covering at a large hospital to see how it would be received. When I entered the staff lounge that morning, Dr. J., one of the anesthesiologists I was friendly with, was sipping a cup of coffee and reading the morning newspaper. I asked him if he had a minute to give me his thoughts about the new infuser. I reviewed the features and benefits, and before I could ask for his feedback, he called over the Chief of Anesthesia. As Dr. J. explained the product to him, he seemed impressed.

The Chief turned to me. "Do you have any literature on this?" I said, "Of course," and handed it to him. He said, "Follow me."

The Chief led me to the O.R. Director's office, where he interrupted her phone conversation.

"Carol, I want one of these in every O.R. this week. I don't care what it costs, and I don't care how you pay for it. Just get it!" He then turned and walked out. I received an order for 11 units by the end of the day.

What made this sale so easy? Urgency! Dr. J. later explained that the Chief had been on call the previous weekend and had multiple trauma surgeries that needed blood transfusions. The transfusions were delayed because the old infusers were slow to inflate and wouldn't hold pressure. Restoring blood volume in a bleeding patient is a matter of life and death. The Chief found a solution to an urgent situation and took immediate action.

In healthcare, urgency gets attention and makes things happen. Getting a sale can be as simple as presenting a scenario and allowing the HCP prospect to sense the urgency. I used the story I shared with you here to create a sense of urgency about replacing old infusers at my other hospital accounts.

MPL insurance matters are almost always urgent for healthcare professionals since a litigation-triggering event could occur at any time. Investing in MPL insurance is not just a business decision but a matter of sleeping well at night, and in the exhausting world of healthcare, sleep is an urgent priority.

|

Written by Mace Horoff of Medical Sales Performance. Mace Horoff is a representative of Sales Pilot. He helps sales teams and individual representatives who sell medical devices, pharmaceuticals, biotechnology, healthcare services, and other healthcare-related products to sell more and earn more by employing a specialized healthcare system. Have a topic you’d like to see covered? Email your suggestions to AskMarketing@ProAssurance.com. |