Market Trends – Hospital M&A Activity

In a world where change is constant, the healthcare system is not immune. Healthcare consolidation continues to impact hospitals and physician practices across the country, ultimately changing the dynamic of how medicine is delivered.

Hospital M&A activity has only become larger, independent physician practices continue to shrink, and services offered by some rural critical-access hospitals, especially in areas related to OB and emergency medicine, are starting to become more obsolete.

The American Medical Association highlights a steady drop in the number of doctors working in private practices since 2012, encompassing fewer than half of physicians in most specialties. For example, only 30.7 percent of cardiologists and 46.9 percent of radiologists are referenced as continuing to work within a private practice setting.

However, some specialties still have a majority in private practice, including orthopedic surgery (54 percent), ophthalmology (70.4 percent), and other surgical subspecialties (51.2 percent). Medicare physician payments were referenced as attributing to destabilizing private practices and access to care, as payments have fallen 33 percent over the past quarter century.

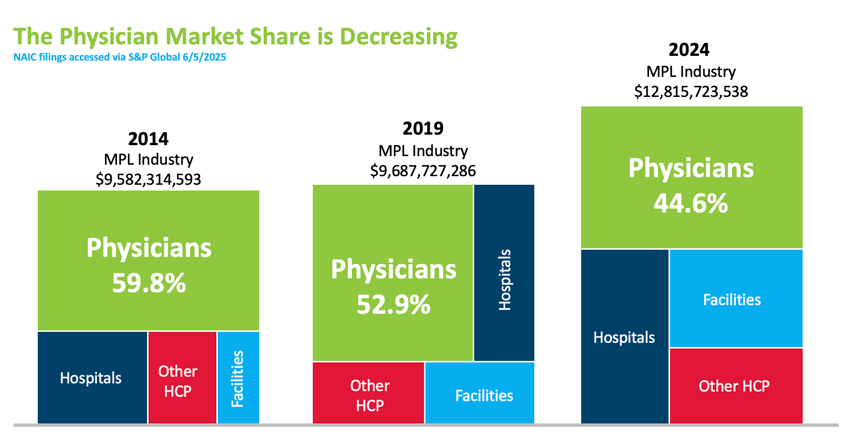

The illustration below shows how the composition of our industry has continued to evolve over the most recent 10 years.

In another study released by the Physicians Advocacy Institute, hospital consolidation is shown as continuing at pre-pandemic levels with the average size of hospital deals increasing by 64 percent over the last nine years. It was also noted that “other” facilities have doubled their market share over the past seven years. The following visual provides an illustration of how the market buyer has shifted, with 77.6 percent of physicians considered employed by hospitals or corporate entities as of 2024.

Despite physician consolidation, ProAssurance stands out as a top-five MPL carrier by market share nationwide. We continue to focus on our healthcare portfolio in the physician space, as well as other specialty divisions within the company such as Miscellaneous Medical, Senior Care, Hospitals, and Alternative Risks. As the market landscape shifts in the future, we will continue offering innovative solutions, stability, and product depth to our policyholders.

The Expanding Role of the Advanced Practice Clinician

The activities and duties a licensed healthcare professional is permitted to perform within a state, along with supervision requirements and authority to administer vaccines and prescribe medications, is known as their “scope of practice.” A key trend we are seeing in modern healthcare today is the rapidly expanding scope of Advanced Practice Clinicians (APCs)—including Nurse Practitioners (NPs), Physician Assistants (PAs), Certified Registered Nurse Anesthetists (CRNAs), and Certified Nurse Midwives (CNMs).

The activities and duties a licensed healthcare professional is permitted to perform within a state, along with supervision requirements and authority to administer vaccines and prescribe medications, is known as their “scope of practice.” A key trend we are seeing in modern healthcare today is the rapidly expanding scope of Advanced Practice Clinicians (APCs)—including Nurse Practitioners (NPs), Physician Assistants (PAs), Certified Registered Nurse Anesthetists (CRNAs), and Certified Nurse Midwives (CNMs).

Historically, APCs were primarily seen in the primary care setting to fill the physician labor shortage. Today, APCs work in a wide range of settings, including hospitals, community clinics, and private practices. In in-patient settings, they increasingly perform advanced clinical roles, specializing in fields such as cardiology, oncology, and dermatology.

Contributing Factors

There are several factors contributing to the expanding scope of practice for APCs.

The Association of American Medical Colleges (AAMC) predicts a significant physician shortage by 2036, and with 1 in 5 Americans projected to be 65 or older by 2030, the demand for healthcare services is increasing. In response, many states are expanding the scope of practice laws for APCs. In fact, 27 states have granted full practice authority to NPs, allowing them to practice, diagnose, and treat patients independently.

Studies suggest that care led by advanced practice nurses can be more cost-effective than physician-led care and may result in greater patient satisfaction and reduced waiting times. In addition, the growth of telehealth and remote patient monitoring, accelerated by the COVID-19 pandemic, has enabled APCs to reach more patients, monitor conditions remotely, and provide access to care, particularly in underserved and rural areas.

Challenges and Controversies

Despite their rapid growth, APCs (specifically APRNs) are the subject of ongoing debate. APRNs often encounter barriers related to provider credentialing, hospital admitting privileges, and reimbursement issues. Physician advocacy groups, such as the American Medical Association (AMA), have also opposed expanding APRN scope of practice, citing concerns over patient safety and cost.

Physicians have raised initial concerns regarding legal exposure and training, according to Becker’s Hospital Review, as well as the ambiguity around the APC’s roles and responsibilities when it comes to patient care.

Risk Mitigation

Wendy Alderman, Senior Risk Management Consultant, notes that understanding each state’s scope of APC practice is a good starting point for risk mitigation, as full practice authority can bring broader exposures. “Of course, the strategies for managing risk and patient safety mirror those used for physicians,” says Alderman. “However, I believe APCs’ exposure is an emerging risk, and time will tell whether the same risks are applicable to them.”

As the APC workforce expands, insurers should stay alert to how these providers are used and ensure that policies align with state laws and actual clinical roles. “Because plaintiffs’ attorneys often name everyone involved in a patient’s care, both APCs and supervising physicians may face equal scrutiny in a lawsuit,” notes Alderman. “Open communication between risk managers and underwriters about provider roles and responsibilities strengthens mitigation strategies and supports sound policies.”

The Future of APCs

The job outlook for APCs is exceptionally strong and will likely continue to outpace other clinical roles in medicine. By 2036, tens of thousands of new nurse practitioners and physician associates will be needed to meet rising healthcare needs. In fact, employment for PAs is expected to grow 28 percent and NPs 46 percent by 2033, far outpacing other professions. Should more states adopt full practice authority for APCs, those numbers will continue to rise. To stay up-to-date on the scope of practice for your state, visit the National Conference of State Legislatures. According to Alderman, effective risk management starts with anticipating issues before they grow, especially as APCs take on a larger share of patient care.

Some states employ a restricted practice model, which prohibits APCs from engaging in the practice of medicine without physician supervision. Other states employ a reduced practice model, which requires that APCs collaborate with physicians in order to engage in the practice of medicine, providing APCs with considerably more autonomy than the restricted practice model. Finally, some states follow the full practice model, which grants certain APCs full authority to engage in the practice of medicine.

|

|

.png?width=300&name=MicrosoftTeams-image%20(28).png)

Gratitude in the Season of Reinvention

For years, medical sales representatives sold directly to doctors and other product end-users. If a doctor requested a product, you received the purchase order, and that was that. Then things began to change. Hospitals realized that giving physicians free rein to use whatever products they wanted was costly, so they established product approval committees to make decisions.

When I entered medical sales, it was because I could speak the clinical language of healthcare professionals. Suddenly, I found myself interacting more with stakeholders who had no interest in discussing clinical issues. They wanted to talk about their business. My initial reaction? "I didn't sign up to have spreadsheet discussions with CFOs and other number-crunchers I didn't know." But I had no choice.

Sound familiar? That's where many MPL agents are today. You've spent years cultivating relationships with physicians and practice managers who called the shots. Now those same stakeholders are employees of a hospital system—or worse, a private equity firm in another state, run by people who've never even met the personnel you know.

The most glaring change for medical reps is that access is more difficult. Why would a doctor spend time with salespeople when the products they use aren't their choice anymore? Sure, they might influence committee decisions, but with limited time, they now choose their battles carefully. Instead of one-on-one conversations, reps face product submission processes where feedback is anything but immediate—and often nonexistent.

If you're feeling frustrated, I get it. But here's the uncomfortable truth: this is the same kind of disruption that separates average salespeople from those who become indispensable.

The Touchpoints Are Changing—Not Disappearing

In medtech, reps learned that instead of just calling on a surgeon, they now have to engage with every member of a value analysis committee. Each stakeholder has different concerns and speaks a different language. Personalizing communication for each individual is no longer optional; it has become the only way to stay relevant.

That same shift is happening now for MPL agents. The titles are different, but the challenge is identical: learning to speak the language of administrators, CFOs, and private equity partners while still connecting with the clinicians you've always known.

Relearning Is Painful—Until It Starts Working

The biggest barrier isn't knowledge—it's ego.

I spent decades mastering clinical sales conversations and building relationships with my accounts. However, the market didn't care who I knew or what I liked to discuss; it only rewarded me once I adapted to its needs.

The same principle applies here. Agents who cling to "how it's always been" will fade into obscurity. Those who invest the time to understand new buyers and adapt accordingly will become irreplaceable. The job now is as much about providing insight as it is about offering coverage.

Be Grateful for the Access Your Competitors Don't Have

It's hard to feel grateful in times of forced change, but in a world where access is limited, those who find ways to connect have a true advantage. Be thankful when you get the meeting or when you reach the one person who'll take your call—because if you connect when your competitors can't, you're already winning.

Consolidation doesn't erase opportunity; it just changes where it lives. It rewards those who can:

- Translate old expertise into new conversations.

- Understand the motivations of new decision-makers.

- Bring perspectives others can't.

If you've survived the changes in this industry thus far, that's something to be thankful for. And if you're willing to keep learning and evolving, you can add one more thing to your gratitude list when it's your turn to speak at the Thanksgiving table.

|

Written by Mace Horoff of Medical Sales Performance. Mace Horoff is a representative of Sales Pilot. He helps sales teams and individual representatives who sell medical devices, pharmaceuticals, biotechnology, healthcare services, and other healthcare-related products to sell more and earn more by employing a specialized healthcare system. Have a topic you’d like to see covered? Email your suggestions to AskMarketing@ProAssurance.com. |

Risk Management Updates

Rapid Risk Review Podcast

Latest Episode: A Conversation with Dr. Gita Pensa—Litigation Stress & Physician Burnout

In this episode, guest Dr. Gita Pensa discusses the significant impact of medical malpractice litigation stress on healthcare providers. She explores the psychological and physical effects of litigation stress, the cultural stigma surrounding it, and the changing public perception of physicians, especially post-pandemic. The conversation highlights the increasing burnout among healthcare providers and emphasizes the need for advocacy and collective action to address these challenges. Dr. Pensa shares her personal experiences and insights on how physicians can navigate the complexities of litigation while maintaining their well-being and advocating for systemic change in healthcare.

Allegation

Negligent preparation of surgical site and oxygen administration during surgery alleged in patient injury.

Read the issue

Event reporting is a systematic and timely internal process of reporting occurrences that deviate from expected outcomes. Adverse events include medical errors, near misses, and patient harm obtained as the result of the care delivering process. The benefit of event reporting is to foster a culture of patient safety and provide the opportunity for process improvement.

Watch here

Spoliation is the intentional or unintentional destruction or loss of evidence that may be used in connection with litigation. Learn how spoliation can happen and what you can do to avoid finding yourself the subject of a spoliation jury instruction during a medical malpractice claim.

If you'd like to see more photos, visit the gallery: https://pralinks.proassurance.com/2025LE

Click on "I want to request access." Once you set up your account, you can view our entire photo library from the event.

Women of Influence Reconvenes in Cabo

ProAssurance was delighted to host our second annual Women of Influence event at Leadership Elite in Los Cabos, Mexico. It was a morning filled with networking opportunities and inspiration, thanks to an inspiring session led by Natalie Buccini of Peabody & Buccini LLP, a Registered Nurse and a respected member of ProAssurance’s Defense Panel in California. We look forward to continuing to foster leadership development opportunities throughout the year.

- Communications

- Design

- Digital Marketing